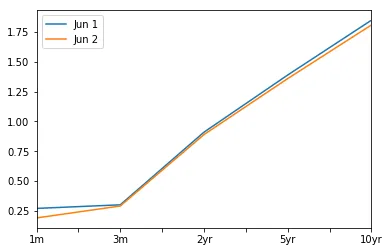

我目前正在尝试构建一个由每日美国国债利率组成的数据框。正如您所看到的,Pandas自动格式化列的顺序,但显然这不是我想要的。以下是我的一些代码。我只需要做一个小例子来展示我遇到的问题。

import quandl

import matplotlib.pyplot as plt

One_Month = quandl.get('FRED/DGS1MO')

^^ 重复适用于所有费率

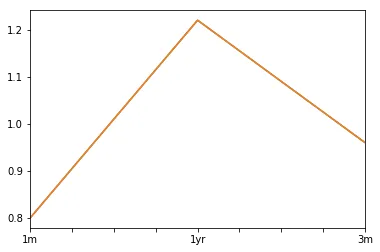

Yield_Curve = pd.DataFrame({'1m': One_Month['Value'], '3m': Three_Month['Value'], '1yr': One_Year['Value']})

Yield_Curve.loc['2017-06-22'].plot()

plt.show()

Yield_Curve.tail()

1m 1yr 3m

Date

2017-06-16 0.85 1.21 1.03

2017-06-19 0.85 1.22 1.02

2017-06-20 0.88 1.22 1.01

2017-06-21 0.85 1.22 0.99

2017-06-22 0.80 1.22 0.96

正如我所说的,我只向数据框添加了三个利率,但显然两年、三年和五年的利率也会导致问题。

我做了一些搜索,并看到了这篇帖子: 绘制国库收益率曲线,如何使用matplotlib叠加两个收益率曲线 虽然上一篇帖子中的代码明显有效,但我更愿意保留我的当前数据集(One_Month,Three_Month...)来完成这项工作,因为我还将它们用于其他分析。

问题:有没有办法锁定列顺序?

感谢您的帮助!