关于绘制置信区间有很多答案。

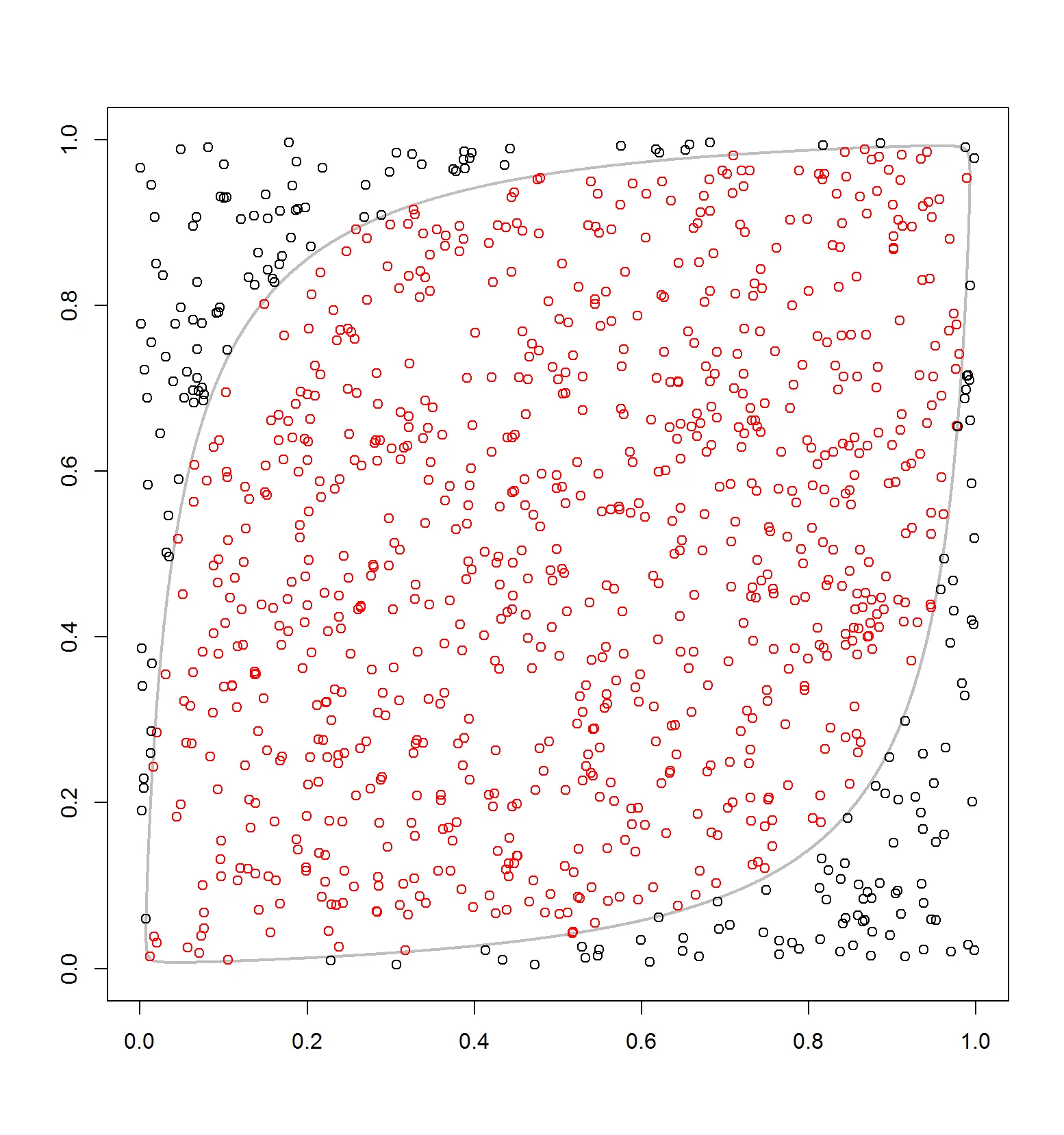

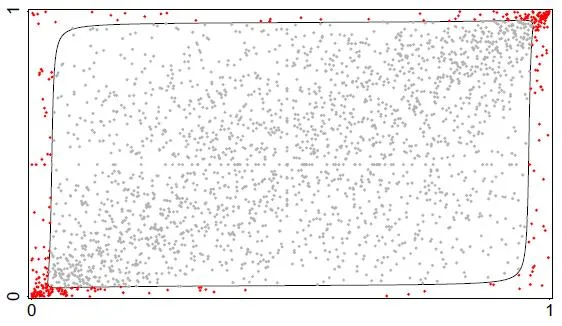

我正在阅读Lourme A. et al (2016)的论文,我想像该论文中的图2一样绘制90%置信边界和10%异常点: 。

。

我不能使用LaTeX并插入定义置信区域的图片:

library("MASS")

library(copula)

set.seed(612)

n <- 1000 # length of sample

d <- 2 # dimension

# random vector with uniform margins on (0,1)

u1 <- runif(n, min = 0, max = 1)

u2 <- runif(n, min = 0, max = 1)

u = matrix(c(u1, u2), ncol=d)

Rg <- cor(u) # d-by-d correlation matrix

Rg1 <- ginv(Rg) # inv. matrix

# round(Rg %*% Rg1, 8) # check

# the multivariate c.d.f of u is a Gaussian copula

# with parameter Rg[1,2]=0.02876654

normal.cop = normalCopula(Rg[1,2], dim=d)

fit.cop = fitCopula(normal.cop, u, method="itau") #fitting

# Rg.hat = fit.cop@estimate[1]

# [1] 0.03097071

sim = rCopula(n, normal.cop) # in (0,1)

# Taking the quantile function of N1(0, 1)

y1 <- qnorm(sim[,1], mean = 0, sd = 1)

y2 <- qnorm(sim[,2], mean = 0, sd = 1)

par(mfrow=c(2,2))

plot(y1, y2, col="red"); abline(v=mean(y1), h=mean(y2))

plot(sim[,1], sim[,2], col="blue")

hist(y1); hist(y2)

参考文献。Lourme, A.,F. Maurer(2016)在风险管理框架中测试高斯和学生t簇的方法。经济建模。

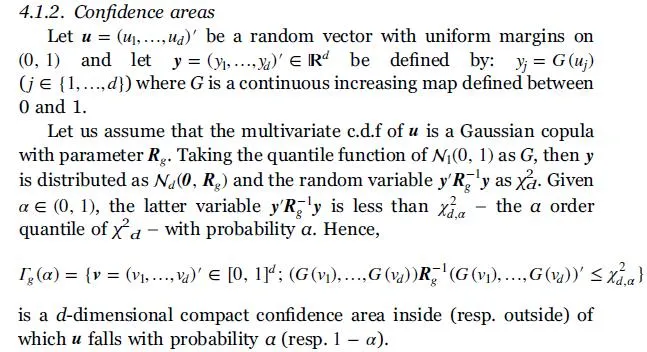

问题。 有人可以帮助我解释方程中变量v =(v_1,...,v_d)和G(v_1),...,G(v_d)吗?

我认为v是非随机矩阵,其尺寸应为$k^2$(网格点)乘以d = 2(维度)。例如,

axis_x <- seq(0, 1, 0.1) # 11 grid points

axis_y <- seq(0, 1, 0.1) # 11 grid points

v <- expand.grid(axis_x, axis_y)

plot(v, type = "p")