我有一个数据集,我知道它服从帕累托分布。请问有人能指点我如何在Scipy中拟合这个数据集吗?我运行了下面的代码,但我不知道返回给我的是什么(a、b、c)。此外,在获得a、b、c之后,我该如何使用它们计算方差?

import scipy.stats as ss

import scipy as sp

a,b,c=ss.pareto.fit(data)

我有一个数据集,我知道它服从帕累托分布。请问有人能指点我如何在Scipy中拟合这个数据集吗?我运行了下面的代码,但我不知道返回给我的是什么(a、b、c)。此外,在获得a、b、c之后,我该如何使用它们计算方差?

import scipy.stats as ss

import scipy as sp

a,b,c=ss.pareto.fit(data)

在拟合幂律函数时一定要非常小心!! 许多所报道的幂律函数实际上是错误地拟合成了幂律函数。详见Clauset等人的论文(如果您没有期刊访问权限,论文也在arxiv上)。他们有一个伴随网站链接到Python的实现。不确定是否使用Scipy,因为我最近使用它们的R实现。

这是一个快速编写的版本,参考了Rupert提供的参考页面。目前在scipy和statsmodels中正在进行工作,并需要使用MLE来处理一些固定或冻结的参数,这仅在主干版本中可用。目前还没有参数估计或其他结果统计量的标准误差可用。

'''estimating pareto with 3 parameters (shape, loc, scale) with nested

minimization, MLE inside minimizing Kolmogorov-Smirnov statistic

running some examples looks good

Author: josef-pktd

'''

import numpy as np

from scipy import stats, optimize

#the following adds my frozen fit method to the distributions

#scipy trunk also has a fit method with some parameters fixed.

import scikits.statsmodels.sandbox.stats.distributions_patch

true = (0.5, 10, 1.) # try different values

shape, loc, scale = true

rvs = stats.pareto.rvs(shape, loc=loc, scale=scale, size=1000)

rvsmin = rvs.min() #for starting value to fmin

def pareto_ks(loc, rvs):

est = stats.pareto.fit_fr(rvs, 1., frozen=[np.nan, loc, np.nan])

args = (est[0], loc, est[1])

return stats.kstest(rvs,'pareto',args)[0]

locest = optimize.fmin(pareto_ks, rvsmin*0.7, (rvs,))

est = stats.pareto.fit_fr(rvs, 1., frozen=[np.nan, locest, np.nan])

args = (est[0], locest[0], est[1])

print 'estimate'

print args

print 'kstest'

print stats.kstest(rvs,'pareto',args)

print 'estimation error', args - np.array(true)

import openturns as ot

data = [

[2.7018013],

[8.53280352],

[1.15643882],

[1.03359467],

[1.53152735],

[32.70434285],

[12.60709624],

[2.012235],

[1.06747063],

[1.41394096],

]

sample = ot.Sample([[v] for v in data])

distribution = ot.ParetoFactory().build(sample)

当然可以打印它:

print(distribution)

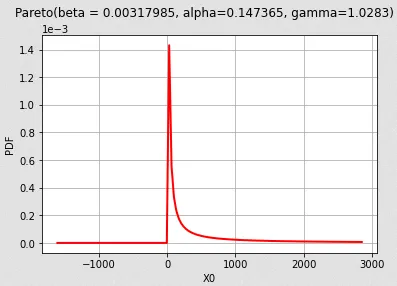

>>> Pareto(beta = 0.00317985, alpha=0.147365, gamma=1.0283)

或绘制其概率密度函数:

from openturns.viewer import View

pdf_graph = distribution.drawPDF()

pdf_graph.setTitle(str(distribution))

View(pdf_graph, add_legend=False)

有关ParetoFactory的更多详细信息,请参阅文档。

distribution = ot.ParetoFactory.build(data)。其次,我收到了一个 TypeError:Wrong number or type of arguments for overloaded function 'ParetoFactory_build'。 看起来 Openturns 库想要一个特定的格式来处理'sample',但我不明白应该如何格式化。 - Tropiliodistribution = ot.ParetoFactory().build(data)。我已经更正了上面的代码。为了被OpenTURNS库理解,样本应该被形状化(大小,维度)。在我的例子中它是(10,1)。 - Jean A.在将数据传递给OPENTURNS中的build()函数之前,请确保按照以下方式进行转换:

data = [[i] for i in data]