虽然这里有很多好的答案,但我会包括一个更加定制化的ECDF图

生成经验累积分布函数的值

import matplotlib.pyplot as plt

def ecdf_values(x):

"""

Generate values for empirical cumulative distribution function

Params

--------

x (array or list of numeric values): distribution for ECDF

Returns

--------

x (array): x values

y (array): percentile values

"""

x = np.sort(x)

n = len(x)

y = np.arange(1, n + 1, 1) / n

return x, y

def ecdf_plot(x, name = 'Value', plot_normal = True, log_scale=False, save=False, save_name='Default'):

"""

ECDF plot of x

Params

--------

x (array or list of numerics): distribution for ECDF

name (str): name of the distribution, used for labeling

plot_normal (bool): plot the normal distribution (from mean and std of data)

log_scale (bool): transform the scale to logarithmic

save (bool) : save/export plot

save_name (str) : filename to save the plot

Returns

--------

none, displays plot

"""

xs, ys = ecdf_values(x)

fig = plt.figure(figsize = (10, 6))

ax = plt.subplot(1, 1, 1)

plt.step(xs, ys, linewidth = 2.5, c= 'b');

plot_range = ax.get_xlim()[1] - ax.get_xlim()[0]

fig_sizex = fig.get_size_inches()[0]

data_inch = plot_range / fig_sizex

right = 0.6 * data_inch + max(xs)

gap = right - max(xs)

left = min(xs) - gap

if log_scale:

ax.set_xscale('log')

if plot_normal:

gxs, gys = ecdf_values(np.random.normal(loc = xs.mean(),

scale = xs.std(),

size = 100000))

plt.plot(gxs, gys, 'g');

plt.vlines(x=min(xs),

ymin=0,

ymax=min(ys),

color = 'b',

linewidth = 2.5)

plt.xticks(size = 16)

plt.yticks(size = 16)

plt.xlabel(f'{name}', size = 18)

plt.ylabel('Percentile', size = 18)

plt.vlines(x=min(xs),

ymin = min(ys),

ymax=0.065,

color = 'r',

linestyle = '-',

alpha = 0.8,

linewidth = 1.7)

plt.vlines(x=max(xs),

ymin=0.935,

ymax=max(ys),

color = 'r',

linestyle = '-',

alpha = 0.8,

linewidth = 1.7)

plt.annotate(s = f'{min(xs):.2f}',

xy = (min(xs),

0.065),

horizontalalignment = 'center',

verticalalignment = 'bottom',

size = 15)

plt.annotate(s = f'{max(xs):.2f}',

xy = (max(xs),

0.935),

horizontalalignment = 'center',

verticalalignment = 'top',

size = 15)

ps = [0.25, 0.5, 0.75]

for p in ps:

ax.set_xlim(left = left, right = right)

ax.set_ylim(bottom = 0)

value = xs[np.where(ys > p)[0][0] - 1]

pvalue = ys[np.where(ys > p)[0][0] - 1]

plt.hlines(y=p, xmin=left, xmax = value,

linestyles = ':', colors = 'r', linewidth = 1.4);

plt.vlines(x=value, ymin=0, ymax = pvalue,

linestyles = ':', colors = 'r', linewidth = 1.4)

plt.text(x = p / 3, y = p - 0.01,

transform = ax.transAxes,

s = f'{int(100*p)}%', size = 15,

color = 'r', alpha = 0.7)

plt.text(x = value, y = 0.01, size = 15,

horizontalalignment = 'left',

s = f'{value:.2f}', color = 'r', alpha = 0.8);

plt.title(f'ECDF of {name}', size = 20)

plt.tight_layout()

if save:

plt.savefig(save_name + '.png')

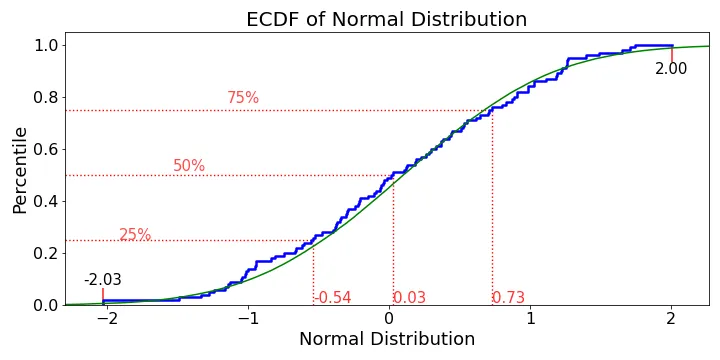

ecdf_plot(np.random.randn(100), name='Normal Distribution', save=True, save_name="ecdf")

额外资源:

yvals=linspace(0,1,len(sorted)),会产生不是真实 CDF 的无偏估计的yvals。 - Daveendpoint = False的linspace,对吗? - hans_meinewhere参数的选择与y参数的定义之间的关系。对我来说最有意义的是使用where=pre和建议的y=np.arange(0,len(x))/len(x),或者您可以使用y=np.arange(1,len(x)+1)/len(x)并使用where=post,但在它们之间切换“where”会(稍微)错误地表示CDF。 - Dave