是否有一个statsmodels API可以从statsmodels时间序列模型中检索预测区间?

目前,我正在使用手动计算预测区间:

这是我的代码。首先,获取一些示例数据...

! python -c 'import datapackage' || pip install datapackage

%matplotlib inline

import datapackage

from statsmodels.graphics.tsaplots import plot_acf

from statsmodels.tsa.api import SimpleExpSmoothing

import statsmodels.api as sm

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

def get_data():

# data licensed for non-commercial use only - https://datahub.io/core/bond-yields-uk-10y

data_url = 'https://datahub.io/core/bond-yields-uk-10y/datapackage.json'

resources = datapackage.Package(data_url).resources

quarterly_csv_url = [pkg for pkg in resources if pkg.name == 'quarterly_csv'][0].descriptor['path']

data = pd.read_csv(quarterly_csv_url)

data = data.set_index('Date', drop=True).asfreq('Q')

return data

接下来,创建一个预测并计算间隔:

data = get_data()

data = data[ data.index > '2005/']

fit = SimpleExpSmoothing(data).fit()

fcast = fit.forecast(1).rename('Forecast')

xhat = fcast.get_values()[0]

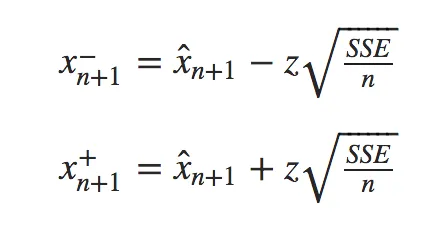

z = 1.96

sse = fit.sse

predint_xminus = xhat - z * np.sqrt(sse/len(data))

predint_xplus = xhat + z * np.sqrt(sse/len(data))

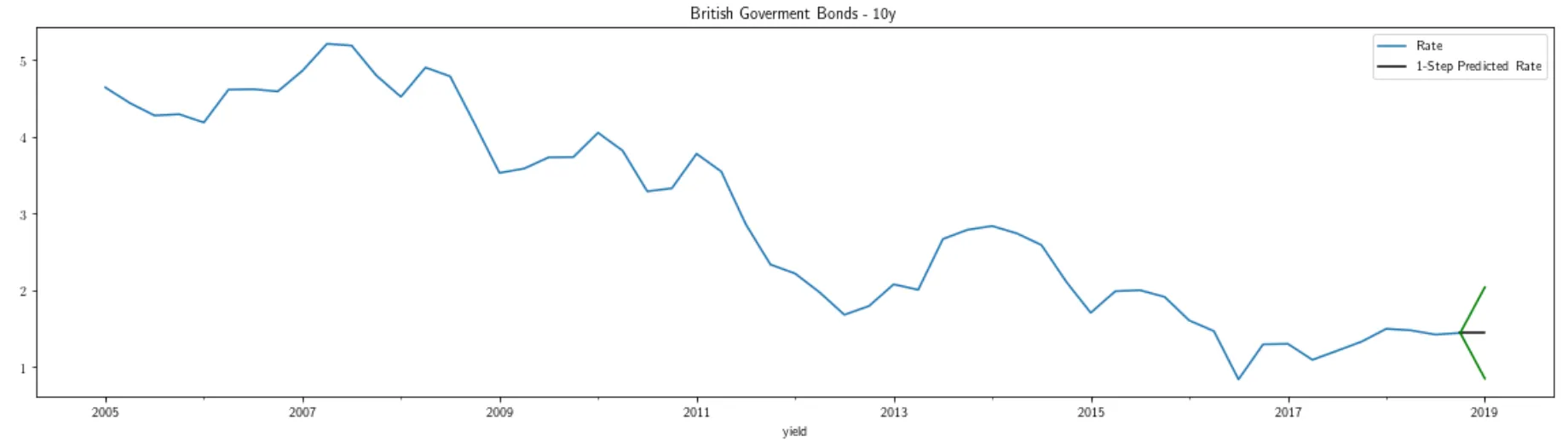

绘制区间...

plt.rcParams["figure.figsize"] = (20,5)

ax = data.plot(legend=True, title='British Goverment Bonds - 10y')

ax.set_xlabel('yield')

#

# 1-Step Prediction

#

prediction = pd.DataFrame(

data = [ data.values[-1][0], xhat ],

index = [ data.index[-1], data.index[-1] + 1 ],

columns = ['1-Step Predicted Rate']

)

_ = prediction.plot(ax=ax, color='black')

#

# upper 95% prediction interval

#

upper_pi_data = pd.DataFrame(

data = [ xhat, predint_xplus ],

index = [ data.index[-1], data.index[-1] + 1 ]

)

_ = upper_pi_data.plot(ax=ax, color='green', legend=False)

#

# lower 95% prediction interval

#

lower_pi_data = pd.DataFrame(

data = [ xhat, predint_xminus ],

index = [ data.index[-1], data.index[-1] + 1 ]

)

_ = lower_pi_data.plot(ax=ax, color='green', legend=False)

我找到了类似的问题,但不是针对时间序列模型: