使用

get_forecast() 方法可以得到时间序列结果,从而获得更加平滑的图形。以下是时间序列的示例:

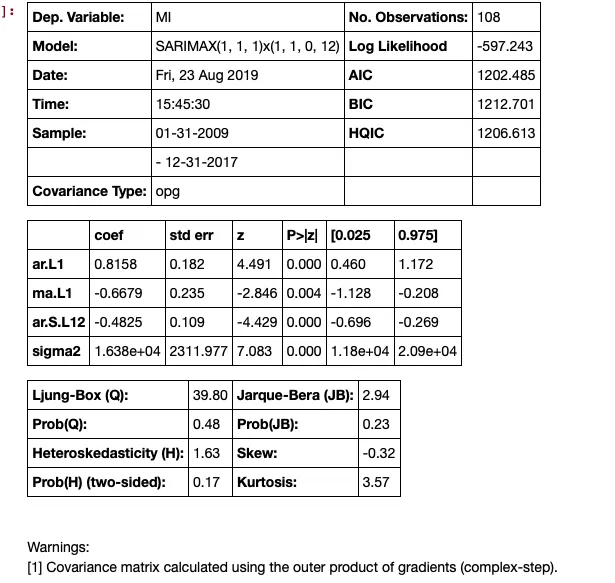

model = SARIMAX(train['MI'], order=(1,1,1), seasonal_order=(1,1,0,12), enforce_invertibility=True)

results = model.fit()

results.summary()

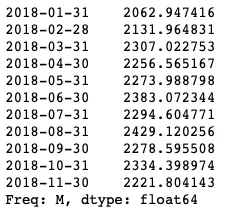

下一步是进行预测,这将生成置信区间。

predictions_int = results.get_forecast(steps=11)

predictions_int.predicted_mean

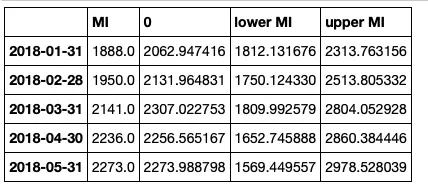

这些可以放在数据框中,但需要进行一些清理:

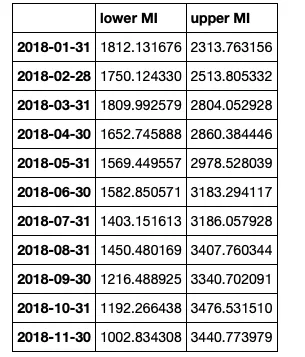

predictions_int.conf_int()

将数据框连接起来,但清理表头

conf_df = pd.concat([test['MI'],predictions_int.predicted_mean, predictions_int.conf_int()], axis = 1)

conf_df.head()

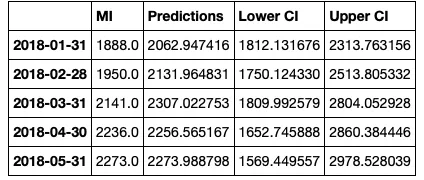

然后我们重命名列。

conf_df = conf_df.rename(columns={0: 'Predictions', 'lower MI': 'Lower CI', 'upper MI': 'Upper CI'})

conf_df.head()

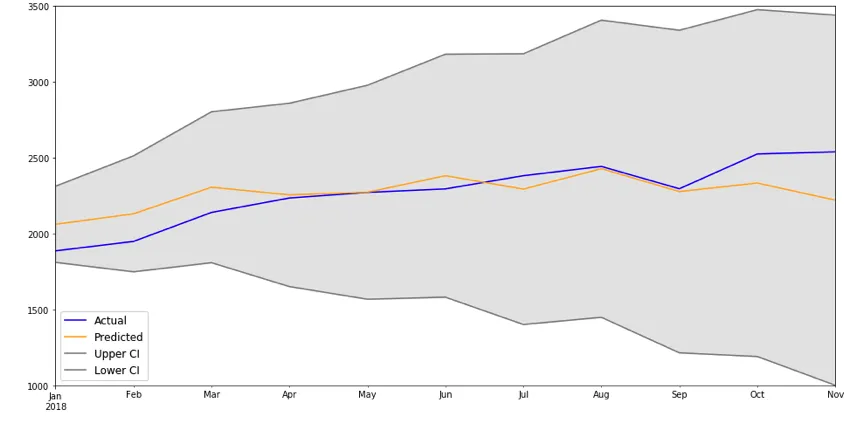

制作图表。

# make a plot of model fit

# color = 'skyblue'

fig = plt.figure(figsize = (16,8))

ax1 = fig.add_subplot(111)

x = conf_df.index.values

upper = conf_df['Upper CI']

lower = conf_df['Lower CI']

conf_df['MI'].plot(color = 'blue', label = 'Actual')

conf_df['Predictions'].plot(color = 'orange',label = 'Predicted' )

upper.plot(color = 'grey', label = 'Upper CI')

lower.plot(color = 'grey', label = 'Lower CI')

# plot the legend for the first plot

plt.legend(loc = 'lower left', fontsize = 12)

# fill between the conf intervals

plt.fill_between(x, lower, upper, color='grey', alpha='0.2')

plt.ylim(1000,3500)

plt.show()