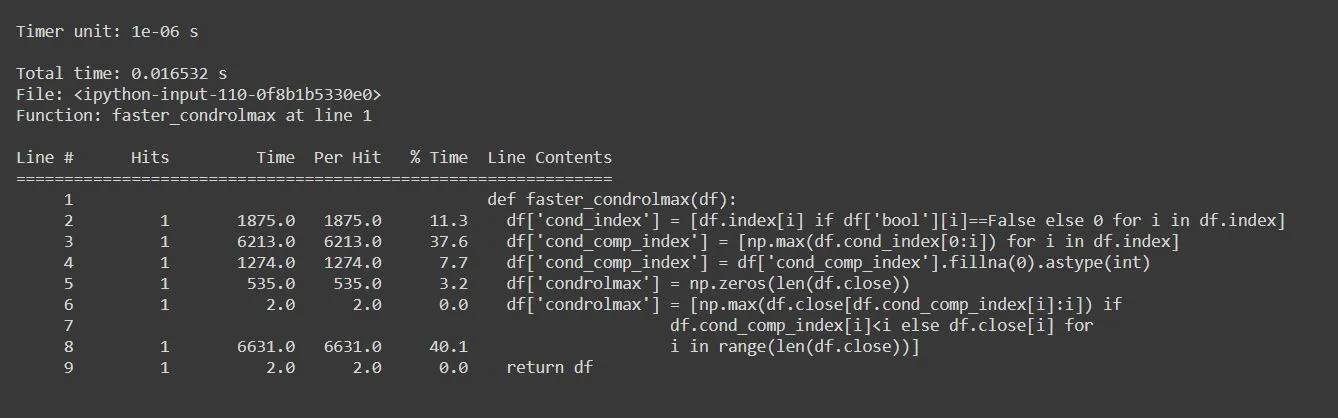

我希望在不使用缓慢的for循环的情况下,能够在列condrolmax(基于列close)中实现以下结果(条件滚动/累积最大值)。

创建此数据帧的代码:

Index close bool condrolmax

0 1 True 1

1 3 True 3

2 2 True 3

3 5 True 5

4 3 False 5

5 3 True 3 --> rolling/accumulative maximum reset (False cond above)

6 4 True 4

7 5 False 4

8 7 False 4

9 5 True 5 --> rolling/accumulative maximum reset (False cond above)

10 7 False 5

11 8 False 5

12 6 True 6 --> rolling/accumulative maximum reset (False cond above)

13 8 True 8

14 5 False 8

15 5 True 5 --> rolling/accumulative maximum reset (False cond above)

16 7 True 7

17 15 True 15

18 16 True 16

创建此数据帧的代码:

# initialise data of lists.

data = {'close':[1,3,2,5,3,3,4,5,7,5,7,8,6,8,5,5,7,15,16],

'bool':[True, True, True, True, False, True, True, False, False, True, False,

False, True, True, False, True, True, True, True],

'condrolmax': [1,3,3,5,5,3,4,4,4,5,5,5,6,8,8,5,7,15,16]}

# Create DataFrame

df = pd.DataFrame(data)

我相信可以对其进行向量化处理(一行代码解决)。有什么建议吗?

再次感谢!

{kind=link}

{kind=link}

{kind=link}

rolling()函数没有提及窗口大小(如果适用),实际上窗口大小可以根据列bool的模式而变化。因此,如果要使用滚动函数,最好使用expanding()而不是rolling()。在这种情况下,在组内使用cummax()会更直接。这就是我们选择cummax()而不是rolling.max()的原因。 - SeaBean