将索引中的整数时间戳转换为DatetimeIndex:

data.index = pd.to_datetime(data.index, unit='s')

这将整数解释为自纪元以来的秒数。

例如,给定

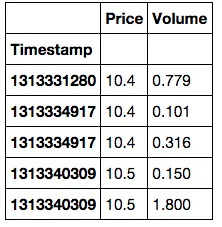

data = pd.DataFrame(

{'Timestamp':[1313331280, 1313334917, 1313334917, 1313340309, 1313340309],

'Price': [10.4]*3 + [10.5]*2, 'Volume': [0.779, 0.101, 0.316, 0.150, 1.8]})

data = data.set_index(['Timestamp'])

data.index = pd.to_datetime(data.index, unit='s')

产量

Price Volume

2011-08-14 14:14:40 10.4 0.779

2011-08-14 15:15:17 10.4 0.101

2011-08-14 15:15:17 10.4 0.316

2011-08-14 16:45:09 10.5 0.150

2011-08-14 16:45:09 10.5 1.800

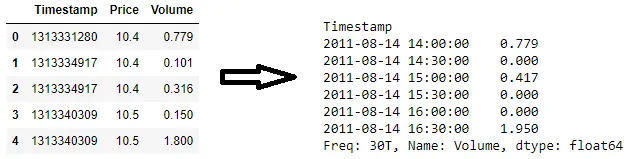

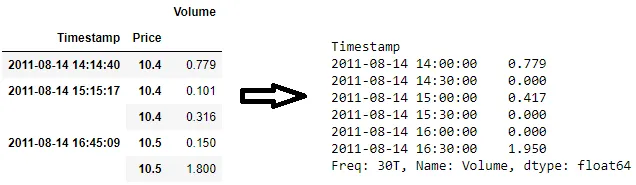

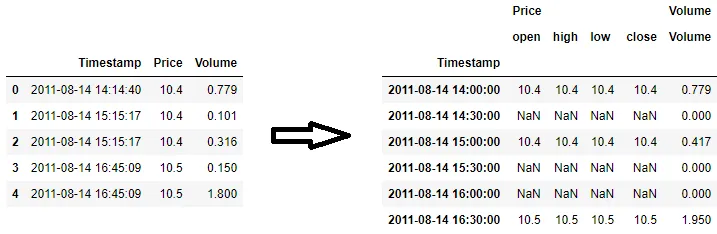

然后

ticks = data.ix[:, ['Price', 'Volume']]

bars = ticks.Price.resample('30min').ohlc()

volumes = ticks.Volume.resample('30min').sum()

可以计算:

In [368]: bars

Out[368]:

open high low close

2011-08-14 14:00:00 10.4 10.4 10.4 10.4

2011-08-14 14:30:00 NaN NaN NaN NaN

2011-08-14 15:00:00 10.4 10.4 10.4 10.4

2011-08-14 15:30:00 NaN NaN NaN NaN

2011-08-14 16:00:00 NaN NaN NaN NaN

2011-08-14 16:30:00 10.5 10.5 10.5 10.5

In [369]: volumes

Out[369]:

2011-08-14 14:00:00 0.779

2011-08-14 14:30:00 NaN

2011-08-14 15:00:00 0.417

2011-08-14 15:30:00 NaN

2011-08-14 16:00:00 NaN

2011-08-14 16:30:00 1.950

Freq: 30T, Name: Volume, dtype: float64